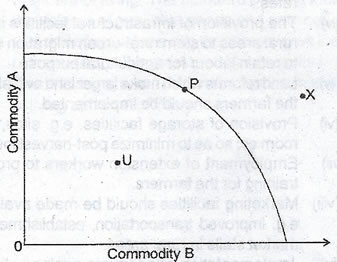

(a) Production possibility curve may be defined as a diagram or graph showing the possible combinations of two commodities that can be produced given a particular amount of resources and level of technology in an economy, within a given period of time.

(b)

P - Resources are fully utilized

U - Resources are under utilized

X - Production is not feasible

(c) (i) An increase in the supply of productive resources e.g. factor inputs, money, time etc.

(ii) Technical progress: improvement in technology through research and development.

(iii) When productive resources are reallocated to the production of the capital goods as against consumer goods.

(iv) Introduction of new ideas or methods.

(v) Human capital development through training and retraining.

(d) The production possibility curve has a negative slope because it illustrates that there is opportunity cost involved in the production of more of one of the commodities.